For many years now, the prospect of a huge and revolutionary new form of aerial transport has been looming. The hybrid airship gains 60% of its lift from helium, but the other 40% is gained aerodynamically. There are many potential applications, such as long-endurance surveillance, airlift into remote locations without runways, and luxury tourism. Operating costs are much lower than conventional aircraft and helicopters. Operating characteristics are much better than conventional airships.

And yet, despite the best efforts of various enthusiastic developers, not a single customer has been secured. There have been many “Letters of Interest” and the like, from armed forces, coastguards, mineral exploitation companies, tour operators and so on. But that elusive first firm order has always been just over the horizon.

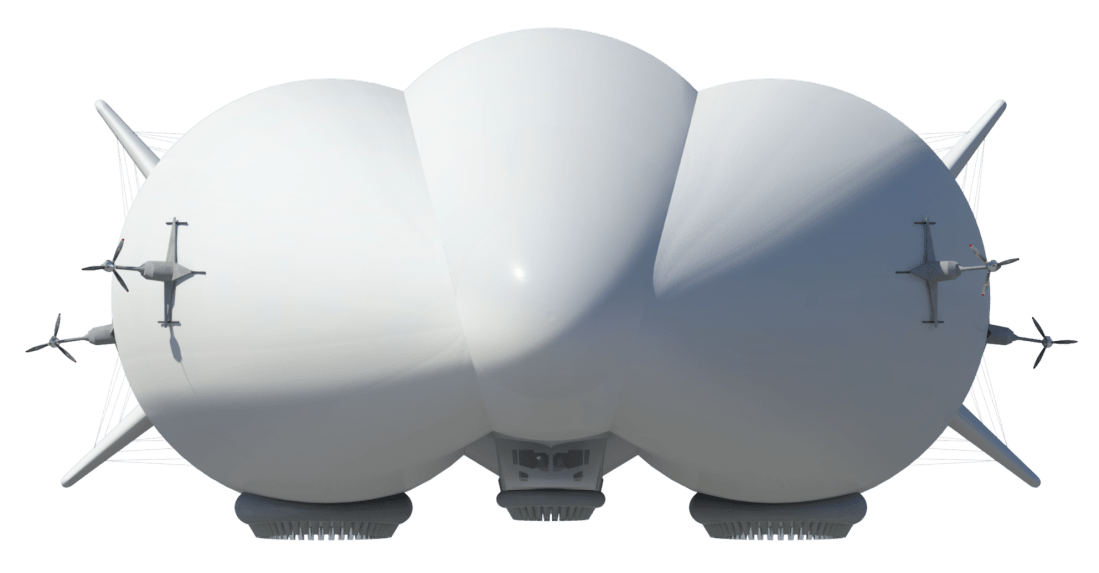

The two most credible projects are the Airlander (above) from Britain’s Hybrid Air Vehicles (HAV), and the LMH-1 (below) from Lockheed Martin in the US. Both companies have sunk large amounts of money into progressing the state-of-the-art, and marketing. HAV claims leadership, having first flown its full-scale design in 2012 as the Long Endurance Multi-Intelligence Vehicle (LEMV) for the US Army. After that programme was cancelled, HAV shipped the prototype to the UK where it was test-flown six times in 2016-17 before the second of two accidents destroyed it. Lockheed Martin flew a subscale prototype back in 2006 but won’t build the real thing without a launch order.

HAV has spent some £50 million on the Airlander since 2012. Some of that came from government grants, and some from loans. But until last year, the majority came from a few key investors, plus £3.3 million from a legion of small shareholders who were attracted by two ‘crowd funding’ rounds. It has been a heroic struggle, that was continued last year largely thanks to a £20 million insurance payout on the lost prototype.

Now, though, HAV needs another £4 million to keep going throughout 2019. It needs much more than that to launch production – assuming that a firm order is achieved. The company says that it is negotiating with a potential “strategic partner” in the aerospace/defence business, who could buy a “substantial” minority stake.

Why should such a partner be interested? HAV says it has developed unrivalled intellectual property and know-how. It has been refining the Airlander design: new engines, fuel tanks, cabin configuration, landing arrangement, and a different configuration of ballonets (the air-filled bags within the envelope whose main purpose is to maintain a constant pressure differential as the helium expands or contracts due to altitude or temperature).

At first glance, HAV and Lockheed Martin are rivals, engaged in a ‘David and Goliath’ struggle. But in practice, they are addressing different markets. The payload of the Airlander is really only 3-5 tonnes, depending on the endurance required (which can be up to five days). That’s enough to carry a good suite of surveillance sensors, or 16 passengers. The LMH-1 is being designed to carry 20 tonnes in a cargo bay that has the same cross-section as a C-130. It is therefore more suited to the “remote lift” market.

I really hope that 2019 brings good news for both these projects. The development of the hybrid airship over the past 25 years is a fascinating story, which I hope to tell in full-length book. And I would like that book to have a happy ending.

Do/would you recommend private – albeit incredibly speculative – investment (via crowd-funding, whatever) in the beast?

LikeLike

I made two small investments in HAV via its crowdfunding. Reluctantly, I decided not to invest again, because of the lack of firm orders.

LikeLike

Chris – great summary article. There are two issues here that may be of interest to explore further:

1) Why have neither LMH-1 nor Airlander secured a customer? They’ve both put huge efforts into this – and LM have put enormous resources behind it (it was one of the entire company’s main focus a couple of years ago) and HAV have had an Airlander flying to demonstrate to customers between 2016 and 2017. Commercially, there is an obvious answer to this:- a minimum 4-5 year build cycle, a minimum 2-3 year test cycle and a possible second build cycle to remove the gremlins of the first build. So 7 years minimum and more likely double that, with a large capital investment upfront, a huge amount of risk and uncertainty and fairly low returns. No rational investor / customer would put money into a venture with those sort of timescales against that return with that risk profile. Therefore, it is a passion project for a billionaire or a Governmental strategic project. It appears only the French Government have publicly stated a cargo-carrying airship is part of their strategic plans and they are backing Flying Whales in that regard, which appears to be very slowly making some progress.

2) The USP of a large airship is remote logistics and cargo. Nothing else can do this role as effectively or as cheaply. This is the Blue Ocean space for lighter-than-air. The issue with long endurance and surveillance roles is that other technologies are improving which are eating into any benefits an LTA solution provides. So drones are getting longer endurance, satellites are getting better and the surveillance kit is getting lighter. By the time a working airship or hybrid is ready, it is likely a better solution will be available using a different technology. The passenger market is about a unique experience and is niche – think helicopters over tourist attractions or what Zeppelin is doing in Friedrichshafen. I understand Zeppelin only just sustains itself even with generous support from the Zeppelin Foundation, and I haven’t met many tourist helicopter operator billionaires.

My conclusion is that a solution for LM or HAV is likely to be a Government-backed remote logistics proposition. There is a logic that discounts any other opportunity. I assume both are chasing that goal, even if they aren’t stating it. Or are they?

LikeLike